Financials Unshackled Issue 20: Weekly Banking Update (UK / Irish / Global Developments)

Perspectives & Snippets on UK / Irish / Global Banking Developments

The material below does NOT constitute investment research or advice - please scroll to the end of this publication for the full Disclaimer

Good morning - and welcome to the latest edition of Financials Unshackled! This note is split into five sections: i) Calendar for the week ahead; ii) Results Recap (key synopsis of results / trading updates / etc. published in the last week); iii) UK Highlights (other key UK sectoral and company developments in the last week); iv) Ireland Highlights (other key Ireland sectoral and company developments in the last week); and v) Other Highlights (select key developments in a Global / European context as well as critical economics / property / politics updates as appropriate).

I hope you enjoy reading it and all feedback is welcome - you can reach me directly at john.cronin@seapointinsights.com.

Calendar for the week ahead:

Mon 18th Nov: UK Finance Card Spending Update for August 2024

Wed 20th Nov: Santander UK 3Q24 Results for the three months to 30th September 2024

Thu 21st Nov: Close Brothers Group (CBG) 1Q25 Trading Update for the three months to 31st October 2024 (07:00 BST) and AGM (11:00 BST))

Thu 21st Nov: Investec (INVP) 1H24 Results for the six months to 30th September 2024 (07:00 BST)

Thu 21st Nov: Together 1Q25 Results for the three months to 30th September 2024 (07:00 BST)

Results Recap

Metro Bank publishes 3Q24 Trading Update

Metro Bank (MTRO) published its 3Q24 trading update for the three months to 30th September on Tuesday last. We get just a few key data points in the 1Q and 3Q trading updates and the following points were noteworthy:

MTRO was profitable in October on an underlying (u/l) basis and the statement also noted that “profits are in line with guidance for 2025 of mid-to-upper single digit RoTE” (all forward guidance conveyed at the stage of the 1H24 results is reaffirmed). We also learned that net interest margin (NIM) came in at 2.48% in October - which was the key highlight (and what underpinned a profitable month) for me in the update. This marks a substantial lift in NIM in a short space of time (NIM printed at just 1.74% in 2Q24) owing to: i) the sale of a £2.5bn residential mortgage portfolio to NatWest Group (NWG) which completed on 30th September; ii) the continued organic reorientation of its asset base to higher-yielding products (including the rolling off the Treasury portfolio); iii) continued focus on extracting cost efficiencies; and iv) the (gradual) grinding down of deposit costs (which peaked in February 2024), which I expect will accelerate in 3Q. This demonstrates that MTRO’s sensible strategy to drive margin accretion and contain costs is working.

Other points of note on the numbers were: i) net loans of £9.1bn were -22% q/q, reflecting the aforementioned portfolio sale; ii) deposits of £15.1bn were -4% q/q, reflecting the continued focus on reducing deposit costs; and iii) the loans to deposits ratio (LTD) has dropped significantly to 60% (from 73% at end-2Q) owing to the portfolio sale. MTRO also notes that it has “a robust pipeline supporting our pivot towards higher yielding commercial, corporate, SME and specialist mortgages”.

See below for further MTRO updates from the last week and you can read the 3Q24 trading update in full here.

UK Highlights

Motor finance remains in the spotlight - and PPI now in focus again too

It was reported last week that the Court of Appeal has refused Close Brothers’ (CBG) and FirstRand’s application for permission to appeal to the Supreme Court in the context of the recent “Hopcraft” judgment - with the Court of Appeal reportedly noting that “it is of the view that there are no arguable grounds for appeal in the present case, which was the clearest possible example of payment of a secret commission to a fiduciary”. The only remaining option now is for the lenders to apply directly to the Supreme Court.

CityA.M. then reported on Wednesday on comments made by Kavon Hussain, Director at Consumer Right Solicitors (CRS) who noted that the “Hopcraft” decision has effectively opened the floodgates - noting that CRS has about 3,000 claims already in the court system and that they expect a few more thousand claims to be lodged in the next 12 months (click here for the article).

Some respite likely to be in the offing as the FCA announced on Wednesday that it is consulting on extending the time motor finance firms have in which to handle commission complaints (read it here) - and also noted that it “…will write to the Supreme Court asking it to decide quickly whether it will give permission to appeal and, if it does, to consider it as soon as possible, given the potential impact of any judgment on the market and the consumers who rely on it”. But concerns are unsurprisingly mounting in relation to the outlook for share buyback programmes in the case of Lloyds (LLOY) and Bank of Ireland Group (BIRG) given the likely prolonged uncertainty around what the ultimate hit to capital will be.

The FCA also noted in its announcement on Wednesday that it is “…considering what impact the Court of Appeal’s judgment has on the review into historical DCAs in motor finance, including for both its timeline and scope. This will inevitably be heavily influenced by any decision of the Supreme Court to hear an appeal and, should it do so, its timelines”. The Telegraph reported later on Wednesday morning (read here) that “…the crucial aspect not revealed in their public announcement, is that the proposed extension applies to motor finance complaints related to all commission types”, which could substantially increase the pool of potential claims to the extent that all car finance deals that included commission become subject to the FCA’s review (though current case law is instructive anyway). To be fair, the FCA does use the word “scope” in its announcement.

And, finally, if you thought things couldn’t get any worse, The Telegraph then reported on Thursday morning that banks are facing the threat of a new £18bn class action lawsuit linked to PPI - noting that “UK law firm Harcus Parker is waiting for the High Court’s permission to launch a group action against high street banks including HSBC, Santander, and Lloyds Bank, accusing them of secretly charging commission to customers on payment protection insurance (PPI) sales. Harcus Parker claims that banks and credit card companies secretly pocketed “extortionate” commission payments of up to 95pc when they sold PPI to customers, an arrangement which they failed to disclose. The law firm is now seeking £18bn in compensation from eight banks and credit card companies, which deny liability.”. Harcus Parker is now reportedly waiting for the High Court’s permission to launch a ‘no win, no fee’ group action against the banks, which is cheaper than bringing claims on an individual basis - with the Court set to make its decision in early 2025. Hard to know how strong the argument is here and, judging by the share price performance of UK banks in the last few days, the market hasn’t taken fright at this - yet at least.

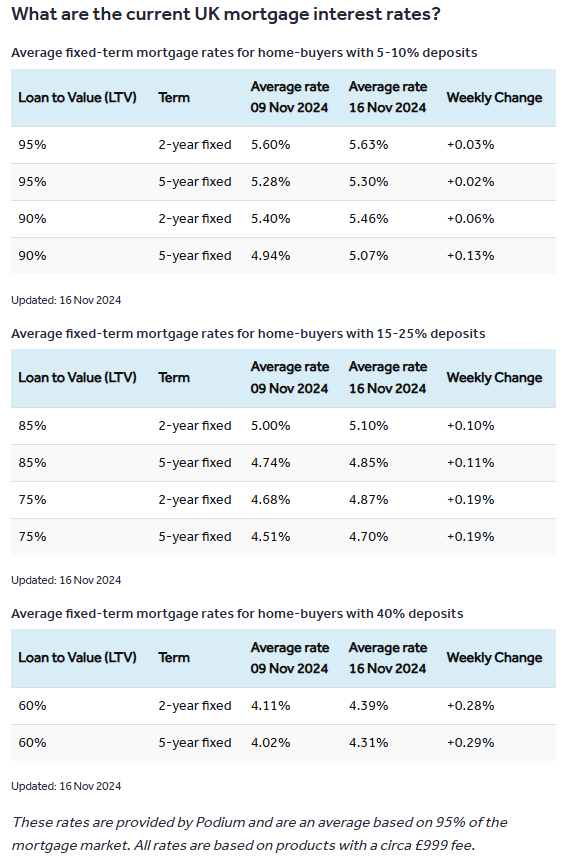

Mortgage rates push up materially

Rightmove published an update on mortgage pricing on Saturday 16th November. It shows that: i) the average price of 90-95% LTV mortgages increased by 2-13bps over the last week; ii) the average price of 75-85% LTV mortgages increased by 10-19bps over the last week; and iii) the average price of 60% LTV mortgages increased by 28-29bps over the last week. This data does not come as a surprise as we have seen a whole host of lenders push through significant rate increases over the last week following the uptick in swap rates (with no sub-4% rates in the market any longer) - but it is interesting to see that the upward rate movements are most pronounced in the lower LTV buckets. These moves are constructive in terms of front book mortgage spread stabilisation (and, potentially, growth). The tables below are extracted from the Rightmove note, which you can read in full here.

It is also worth noting that recent developments are likely to be constructive in an overall net interest margin (NIM) context - savings rates have been falling (see Moneyfacts piece from Tuesday 12th November here and This Is Money piece from the same date here) and are now stagnating, which is constructive in a liability margin context. I have argued before that I don’t see renewed Treasury / FCA pressures in a savings rates context and I remain of that view.

Barclays close to a deal in respect of its merchant acquiring business

Mark Kleinman at Sky News reported on Thursday that Barclays (BARC) is in ongoing detailed discussions with Brookfield in relation to a potential disposal of a c.80% shareholding in its Merchant Acquiring business, though a sale agreement is not thought to be imminent (click here for the article). This news follows a 22nd October article on Sky News (click here to read that article) which noted that the pair were in detailed discussions in relation to a prospective transaction and that a source indicated to the news outlet that the deal structure would involve Brookfield agreeing to bear the costs associated with growing the payments business rather than paying a significant upfront sum. As reported in both articles, estimates in relation to the value of the business have varied widely - ranging from <$1bn to $2.5bn.

Further Updates on Metro Bank

Metro Bank (MTRO) also announced, on the morning of its 3Q24 trading update, that the FCA has imposed a fine of £16.7m on the bank relating to historic deficiencies in transaction monitoring systems and controls - which were identified in April 2019 and fully remediated in 2020. MTRO engaged and co-operated fully with the FCA’s enquiries and accepts its findings. This brings to a close this historical issue (which relates to issues over the June 2016 through December 2020 period when MTRO was run by a different management team) and is helpful in a legacy issue closure context. You can read the MTRO announcement here, the FCA’s announcement here, and the FCA Final Notice here.

MTRO also announced last week that Marc Page’s appointment as CFO has received regulatory approval and that he has now been appointed as an Executive Director and CFO.

Finally, on MTRO, Robert Sharpe (Chair and NED) sold 29,000 shares in the bank at a price of 93.74p per share on Thursday last, netting him proceeds of c.£27k.

Lexham Partners said to be negotiating purchase of Atom Bank stake

Mark Kleinman at Sky News broke a story on Tuesday last noting that a new investment firm, Lexham Partners (established by Dominic Perks), is said to be negotiating the acquisition of c.£3.5m of stock in Atom Bank - at a price of 40p per share (which, the article notes, is consistent with the price at which the November 2023 capital raise was struck at, according to Atom Bank Chairman Lee Rochford), which implies an equity valuation of c.£375m for Atom Bank - and follows its recent inaugural Tier 2 notes issuance. The article also states that Sanjiv Somani, who played a critical role in the launch and initial rapid growth of Chase UK, is a Partner at Lexham and will manage the investment to the extent that the transaction completes. Click here for the article.

This would, in my view, mark an acquisition of a strategic position in the bank by Lexham and its interest is, I suspect, unlikely to stop there. Atom Bank is a unique digital challenger bank that has now proven its ability to eke out profitability by focusing on highly competitive mainstream lending markets. While it doesn’t have a current account proposition, the benefits of Atom’s highly efficient scalable operating model denote substantive operating leverage benefit capture capability. It turned a corner in the 12 months to 31st March 2024, reporting an operating profit of £27m for the year - and what was most interesting for me was that a 16pps reduction in its Cost/Income ratio (CIR) was delivered in FY23 despite net loan growth of +39% y/y, an increase of >10% in average staff numbers, and mid single-digit cost of living-related salary uplifts. Indeed, Atom Bank has grown its loan book to >£4bn in size while maintaining suppressed arrears and forbearance levels - and, notably, it has strategically been developing IRB models for many years (with a remark in its latest Annual Report to the effect that “We will continue to invest in our IRB programme and look to complete delivery of our remaining modules for regulatory assessment in due course”). More scale should be conducive to material returns augmentation despite the evolving rate backdrop - with prospective IRB accreditation also likely to be highly impactful from a returns perspective. It will be interesting to see if this transaction completes as well as understand more about Lexham’s intentions.

Shareholding changes / Director share sales

The government’s shareholding in NatWest Group (NWG) had fallen to just 11.34% by Tuesday 12th November following: i) a further buyback of stock from government (3.16% of the issued share capital) at a price of 380.8p per share; and ii) continued share sales under the ongoing trading plan. Interesting to read Nils Pratley’s take last week in The Guardian on NWG share sales more broadly - and I wholeheartedly agree with his view that “…the plan by the former Tory chancellor Jeremy Hunt to conduct a flashy £3bn sale of shares to the public was always an absurd waste of time and money” (click here to read Pratley’s article). Indeed, the ever-entertaining Alistair Osborne struck a similar tone in his opinion piece in The Times, noting that “a cut-price public sale wouldn’t have helped” imagining that the campaign strapline could have been “Don’t Tell Nige”!

Stephen Dainton, President of Barclays Bank PLC and Head of Investment Bank Management, disposed of 244,885 shares in Barclays (BARC) on Tuesday 12th November at price of 257.9p per share, netting him proceeds of c.£632k. A big sale and, interestingly, this move follows Danny Nealon’s, CEO of Barclays’ (BARC) US Consumer Bank (USCB), disposal of 104,741 shares in BARC at a price of 243.5p per share on Monday 4th November, netting him c.£255k.

Jen Tippin, Group COO of NatWest Group (NWG), sold 22,000 shares in NWG at a price of 391.6p per share on Monday last, netting her proceeds of c.£86k.

Snippets

EY UK forecasts a pick-up in growth in net bank loans outstanding to UK households and businesses to +3.7% y/y in 2025 and to +4.3% y/y in 2026 (from +2.6% y/y in 2024). The factors underpinning the acceleration in the pace of growth that EY UK foresees are: i) acceleration in the pace of GDP growth (to 1.5% in 2025 and 1.6% in 2026); ii) easing political uncertainty; iii) lower interest rates and stabilising inflation supporting affordability / investment; and iv) steady wage growth. EY UK also expects that default rates will stabilise (indeed mortgage arrears have inflected, according to recent UK Finance data - and are now on a downward path). The lending growth estimates sit significantly above current consensus expectations. Click here for the EY UK note.

Lots of media coverage last week on the Chancellor’s comments to the effect that regulation has “…gone too far”. You can read her Mansion House speech here, which touches on what changes are afoot in a regulatory change context. Her letter to the Prudential Regulation Committee (PRC) can be found here, her letter to the Financial Policy Committee (FPC) can be found here, and her letter to the FCA can be found here. Indeed, the FCA issued a statement on Friday (following Reeves’ speech) noting that it is committed to supporting growth, which you can access here. Separately, Sky News ran an interesting piece last Monday on how the Treasury is likely to begin a process to recruit the next CEO of the FCA in 1Q25 as Rathi is thought unlikely to seek a second term - and that a new Prudential Regulatory Authority (PRA) CEO will also soon be needed as Sam Woods’ second term expires in mid-2026 (click here for the article).

Following Tulip Siddiq’s (Economic Secretary to the Treasury) 14th October issuance of a statement confirming that the government would bring forward legislation to implement reforms to the ring-fencing regime as soon as parliamentary time allows, the Treasury published, on Monday last, the response to its Consultation on near-term reforms (click here for the document) and laid in Parliament the final Statutory Instrument to reflect the necessary changes to address the issues raised by the respondents. These changes are helpful for Chase UK (J.P.Morgan) particularly - and also for Marcus (Goldman Sachs) which is now understood to be essentially just a funding vehicle for the wider business. Click here for the release.

The FCA and Financial Ombudsman Service (FOS) have published a joint call for input to seek views on how to modernise the redress system and intend to present proposals in 1H25 - read about it on the FCA website here.

Nikhil Rathi, FCA CEO, has said the FCA will present revised fundamentally reshaped proposals “in the next week or so” in relation to its plans to ‘name and shame’ companies that are the subject of FCA investigations. This is welcome in my view. FT article on this here.

Bloomberg reported last week that the FCA is in talks with private credit players to understand the oversight and governance of the different valuation methodologies used by these lenders, according to sources. The article further notes that one of the sources informed the news agency that the FCA plans to publish its interim findings by the end of 2024. Click here for the article.

Jemma Slingo at Investors Chronicle penned a piece on how structural hedges work on Wednesday last which you can read here. This follows a recent article in This Is Money on how the hedges work and how they are providing strong net interest income (NII) tailwinds for select UK banks - you can read that article here. If interested in reading more on structural hedging, I recommend consulting: i) a presentation from RBS Treasury dated 13th June 2018 (click here for it); and ii) the presentation (click here) and the associated management walkthrough document (click here) from Barclays’ Structural Hedge Teach-In session held on 28th November 2023.

Miguel Sard, Chief Banking Officer for Retail at Shawbrook, commented during the week at a London conference held by The Mortgage Lender (which is owned by Shawbrook) that he anticipates more consolidation activity in the mortgage market as lenders fall into “trouble” (he was presumably referring to specialist lenders): “I can see some pieces of organisations being sold to others”. The comments were reported by Mortgage Solutions and you can access the article here.

Lloyds (LLOY) issued a RNS on Thursday noting that it has now completed the £2.0bn share buyback programme which it announced on 23rd February - at an average price of 55p per share. Click here for the RNS.

Nationwide appointed David Bennett (Chair of Virgin Money UK) as NED with effect from 13th November. Read the RNS here.

Ireland Highlights

No placing of AIB Group stock last week

Maybe it’s just too close to the General Election to grab the Finance Minister’s attention - or seen as too politically risky / sensitive depending on what government has in mind - but I have to admit I was a little bit surprised that the government didn’t elect to place more stock in AIB Group (AIBG) last week given the strong recent share price performance. That said, I can see how landing another big cheque in the days immediately preceding a General Election could be seen as maximising political capital so maybe a placing is on the agenda this week (or even early next week). The share price stood at 543c at Friday’s close, which is well north of the price at which the last placing was executed (at a price of 492.4c per share). That, in and of itself, should give the Finance Minister confidence to transact - and, for what it’s worth, based on the demand for previous placings there has to be a temptation, at this stage, to sell a (potentially much) bigger block the next time the government transacts. That’s what I think they should do - upsize, accelerate the exit, and it’s a nice further boost to the public purse ahead of a General Election. But, that said, if government is thinking about doing a larger trade maybe they’ll wait until post-Election so as to avoid any hostile public reaction to the implications that would mean for banker compensation. Appreciate I’m in the zone of deep speculation here but it’s one to keep an eye on all the same and let’s see what the next week or so brings. My gut view is that there will be a placing pre-Election though I’m not convinced it will be of much larger size than what has gone before.

CBI Retail Interest Rates show favourable volume and pricing trends

The Central Bank of Ireland (CBI) published its monthly Retail Interest Rates update for September 2024 on Wednesday 13th November. Click here to read the release. All in all, the data point to pretty favourable volume and pricing conditions for the banks. Key points:

The weighted average interest rate on new Irish mortgage agreements in September was 4.08% (-3bps m/m, -22bps y/y) - marking the first y/y reduction since 2022, though average rates are now 49bps higher than the euro area average (up from 40bps higher in August), meaning Ireland remains 6th highest in the euro area for mortgage originations pricing. This isn’t getting much attention in the run-up to the General Election (to be held on Friday 29th November) and I suspect the political system is unlikely to apply any great pressure on the banks in this vein in the relative near-term.

The volume of new mortgage originations was +30% y/y in September to €930m, reversing the 14% y/y reduction seen in August (renegotiated agreements were +66% m/m to €229m, reversing the 14% m/m reduction observed in August).

Fixed rate mortgages represented 70% of the volume of new mortgage agreements in September with standard variable rate comprising the residual 30% (the take-up of variable product has ratcheted up significantly in recent times as consumers expect official rate reductions to translate into lower pricing).

The interest rate on new consumer loans increased by 18bps y/y (+4bps m/m) to 7.74% in September. The total volume of new consumer loans was €214m in September, down from €230m in August - and -2.7% y/y. However, it must be noted that the pricing on, and volume of, new consumer loans can fluctuate quite wildly on a monthly basis.

Following a strong surge in new NFC (non-financial corporate) borrowing in July (with €1.8bn of loan agreements struck, up from just €595m in June) we saw NFC borrowing fell back to €1.2bn in August. However, new NFC lending picked up significantly again in September to €2.4bn (notably +124% y/y). The weighted average interest rate on new lending was —161bps m/m to just 4.08% in September (which is below the average euro area equivalent rate - of 4.67% - for the first time in the series). Again, volumes and pricing can ‘ebb and flow’ quite significantly m/m so I would not call out a particular pricing trend based on one month of data.

The average rate on household overnight deposits remained unchanged m/m at 0.13% in September 2024 while the average rate on NFC overnight deposits reduced by 2bps m/m to just 0.12%. The majority of listed Irish banks’ customer funding sits in current accounts so this data, once again, illustrates the enormous liability margin benefits that the listed banks have enjoyed since official rates started to rise. The weighted average interest rate on new household agreed maturity deposits and new NFC term deposits was +1bp m/m to 2.63% and -35bps m/m to 2.75% respectively in September. These rates are considerably lower than the average euro area rates (of 2.98% for new household agreed maturity deposits and 3.28% for new NFC agreed maturity deposits).

Snippets

BlackRock’s shareholding in Bank of Ireland Group (BIRG) reduced further to 7.51% following a transaction on Thursday 14th November (previously disclosed shareholding: 7.99%). BlackRock has recently been upsizing its shareholding in AIB Group (AIBG).

The Wall Street Journal picked up last week on a recent J.P.Morgan research report on Irish banks in which the analysts note that the status quo is unlikely to change given the weak polling trends for Sinn Fein ahead of the 29th November General Election - a view that regular readers will be aware that I concur with. Indeed, the findings of the latest Irish Times/Ipsos B&A poll (from Thursday 14th November) show that Fine Gael and Fianna Fail commanded a combined 44% (25% and 19% respectively) with Sinn Fein at 19% - meaning a rerun of the current Coalition government (perhaps minus the Green Party) appears to be the most likely outcome, which will be a relief (though not unexpected at this stage) for the banking sector. The analysts also note that AIB Group (AIBG) and Bank of Ireland Group (BIRG) are expected to continue to operate in a favourable macro environment and prefer AIBG to BIRG: “We see AIBG better positioned to benefit from improving volume and migration trends compared to BIRG which continues to reduce U.K. exposure, thereby limiting group-level loan growth”. Note that JPM is corporate broker to AIBG. As an aside, in a macro context it’s also worth noting that S&P Global Ratings upgraded Ireland’s Outlook to “Positive” (from “Stable”) on Friday last - while Fitch affirmed its ratings at AA with a “Stable” Outlook. If you want to read more on the macro then AIB’s economic update presentations are always a useful run-through and the latest one from Friday last can be located here - and, for more, see the NTMA’s latest detailed investor presentation from 18th October here.

The Business Post reported last week on a survey conducted by Revolut Business which has reportedly found that 72% of Irish business leaders believe that traditional banks are too slow in addressing their financial needs compared with 64% of business leaders across Europe as a whole. While the findings might be somewhat self-serving from Revolut’s perspective, they do illustrate that the market perceives there to be a gap in a bank quality of service context. Indeed, one wonders what the legacy of those current bank management teams who fail to adequately invest in technologies will be years from now when newcomers or the likes of Chase’s digital initiative begin to disrupt in earnest. Click here for the article.

An interesting detailed article on the Irish motor finance market featured in Motor Finance Online on Wednesday 13th November - and I was delighted to contribute to the piece. It picks up on how 2024 has been a challenging year but industry figures are positive in relation to the outlook. You can read it here.

The Business Post reported on Tuesday that the Dutch neobank Bunq is launching an investment account for Irish customers that will enable them to trade in fractional shares. The move is seen as a counter to Revolut’s offering to its Irish customer base (notably, the article picks up on Revolut data which show that the average value of its Irish customers’ investment portfolios is just €2,600 versus an average of €4,000 across its entire European customer base - so, perhaps it’s a good time for some challenge then). Click here for the article.

The Governor of the Central Bank of Ireland (CBI) Gabriel Makhlouf penned a blog on Thursday last on the CBI’s Strategy 2024 document - which was published last month. He speaks about transforming how the CBI regulates and supervises the financial system, how the Fitness & Probity regime is set to be reformed, and on the recently established innovation sandbox programme - amongst other matters. You can access the blog here and the Strategy 2024 document here.

David Duffy is back in Ireland following the completion of Nationwide’s acquisition of Virgin Money UK and did an interview with Jon Ihle of The Sunday Times, which was published in the newspaper yesterday. While Duffy is turning his immediate attention to his upcoming Camino voyage it will be interesting to see where he crops up next with plenty of offers of domestic and overseas non-executive roles and other gigs undoubtedly set to cross his desk. Click here to read the interview.

Other Highlights

Analysts reflect on European banks’ outperformance

The Wall Street Journal picked up on a few interesting analyst reports last week. Firstly, the newspaper reports on a recent Jefferies note which, reportedly, states that European banks reported an aggregate 8% PBT beat in 3Q24 (with stronger revenue, lower provisions and costs underpinning the growth) - and, reportedly, going on to observe that “European banks have now outperformed consensus expectations for no less than 17 quarters in a row”. The newspaper also flags recent J.P.Morgan research which reportedly notes that the analysts at that firm prefer European investment banks to US investment banks given that “the market seems to have already priced in potential positive moves by the new administration in their valuations of U.S. lenders but not in that of European ones” - reportedly noting that its top picks are Deutsche Bank, UBS and Barclays (BARC).

Outside of just the investment banks, there is a substantial (seemingly structural) disparity between the multiples of tangible book value at which US and European banks trade and it seems there are sound arguments to the effect that some of the factors underpinning the disparity in trading multiples are overcooked in the US banks’ favour (which is not to offer a view on when or if the market will adjust its thinking on European bank valuations). I will explore this theme in some depth soon.

Snippets

The European Banking Authority (EBA) published the methodology, draft templates and key milestones for its 2025 EU-wide stress test on Tuesday 12th November and you can locate all the documents here. The stress test exercise will formally commence in January 2025 following the release of the macroeconomic scenarios (which have not yet been published) - and results are scheduled for publication in early August 2025. A common macroeconomic baseline scenario and a common adverse scenario will be run for the 2025 through 2027 period - and the usual static Balance Sheet assumption will apply. For clarity, there is no mention of climate stress testing in the methodology document.

The ECB’s latest Supervision Newsletter was published on Wednesday last. It includes an interview with Christine Lagarde (President of the ECB) reflecting on 10 years of European bank supervision; ii) challenges and solutions in the context of banks collecting energy performance data for real estate; iii) good practices identified by the ECB for stress-testing, governance, forecasting and outflow management in a liquidity context; iv) the findings of an ECB review which point to a struggle on the part of the banking sector to capture risks pertaining to, and to identify exposures relating to, private equity and credit fund exposures; v) the ECB’s findings that banks’ progress on data quality management continues to be insufficient and that banks need to invest further in IT and cyber resilience; and vi) how less significant institutions (LSIs) have recovered strongly in 2023/24. All articles can be located here along with a fresh set of NPL indicators which show that NPL ratios for loans to non-financial corporates (NFCs) collateralised by commercial property have inflected from their historical low of 4.05% in 1Q23, reaching 4.61% in 2Q24.

Bloomberg reported last Tuesday that the ECB plans to demand more information from banks in relation to their geopolitical risk exposures. Click here for the article.

Bloomberg published an interesting piece last week noting how high demand for AT1 instruments is allowing banks to incorporate more clauses to give them flexibility over when and how they redeem the existing bonds. Clean-up call options have been included in more than 40% of European AT1 bond issuance terms in 2024, according to data compiled by Bloomberg - these allow lenders to hoover up the bonds that remain outstanding after a buyback. These enhanced terms effectively just reflect the significant growth in investor demand for AT1 paper since the market settled subsequent to the Credit Suisse saga in the Spring of 2023 (it is also worth noting, in this vein, that Bloomberg also reported last month that some investors have been switching out of AT1 into Tier 2 of late given the narrowing in spreads between the two instruments). Click here for the article.

Excellent lengthy article on Bloomberg on Thursday on SRTs (US context) which you can read here. Hard to disagree with Scott Goodwin of Diameter Capital Partners’ view to the effect that “SRTs are a win-win for banks and investors” with banks able to use the capital released to grow their balance sheets while investors attain attractive returns on high-quality assets. Indeed, I recently wrote on S&P Global Ratings’ view that “…SRT issuance will grow and become broader based as further banks look to manage their credit portfolios more actively through the implementation of the final Basel III standards”, remarking that this seemed a sensible conclusion given the disparity between the market and the regulatory view of risk in the context of certain high risk-weighted loan assets - with SRTs effectively a means of arbitraging between the two to procure capital efficiency optimisation.

Interesting Bloomberg Odd Lots podcast on the relationship between banks and private credit - with Steven Kelly, Associate Director of Research at the Yale Program on Financial Stability, offering his perspectives. Kelly notably calls out the BoE for its stronger level of supervision (relative to the US) in an overall systemic context: “So generally this stuff goes better in foreign countries than it does in the US, particularly the Bank of England. They have like a system-wide stress test now where they simulate shocks in theory through like the whole financial system. They're big on macro-prudential stuff over there.”. Click here to listen back and/or for the transcript.

Chase’s Teresa Heitsenrether opines to The Financial Brand that the AI revolution will be won by the large incumbent banks “with the deepest data troves that can fuel the latest tools”. You can read it here.

ING’s Bank Outlook 2025 was published on Wednesday last. It’s a useful read and you can get it here.

Interesting feature in the FT on Friday on Sebastien Siemiatkowski, the Klarna CEO (read it here) - following the company’s confirmation last week that it has filed IPO documents in the US (with valuation ambitions thought to be in the $15-20bn range). You can read more about the prospective IPO in the FT here.

BoE Governor Andrew Bailey spoke on the topic of growth at the Mansion House Financial and Professional Services Dinner on Thursday last. He concludes by noting: “Potential supply and growth matter a lot. We don’t have a good recent inheritance, so this is a big issue that needs our attention. Investment and capital formation, and how to increase it matter. So does labour supply in the face of an ageing population and an immediate question of participation. We can and should measure things better and we could try answering the phone to the ONS. We must do what we sensibly can to preserve safe openness of the economy. AI has a lot of potential to change the picture, but don’t expect that change to come very quickly. These are very important issues.”. You can read the full speech here.

Disclaimer

The contents of this newsletter and the materials above (“communication”) do NOT constitute investment advice or investment research and the author is not an investment advisor. All content in this communication and correspondence from its author is for informational and educational purposes only and is not in any circumstance, whether express or implied, intended to be investment advice, legal advice or advice of any other nature and should not be relied upon as such. Please carry out your own research and due diligence and take specific investment advice and relevant legal advice about your circumstances before taking any action.

Additionally, please note that while the author has taken due care to ensure the factual accuracy of all content within this publication, errors and omissions may arise. To the extent that the author becomes aware of any errors and/or omissions he will endeavour to amend the online publication without undue delay, which may, at the author’s discretion, include clarification / correction in relation to any such amendment.

Finally, for clarity purposes, communications from Seapoint Insights Limited (SeaPoint Insights) do NOT constitute investment advice or investment research or advice of any nature – and the company is not engaged in the provision of investment advice or investment research or advice of any nature.